The NSE Mauritius Files have triggered renewed scrutiny around the National Stock Exchange of India and its Mauritius-linked shareholding structures ahead of its long-delayed public listing. Questions are being raised regarding beneficial ownership transparency, early offshore stake acquisitions, and extraordinary valuation growth from nearly ₹17,500 crore in 2015 to an estimated ₹5 lakh crore in the unlisted market today. Particular attention has focused on the reported acquisition of NSE shares by DVI Fund Mauritius following a stake sale by IFCI Limited. Investigative concerns presently centre on transparency, regulatory oversight, and whether any offshore structures concealed ultimate economic beneficiaries.

NSE Mauritius Files: ₹5 Lakh Crore Ownership Mystery Raises Questions Before Long-Delayed IPO

India’s largest stock exchange faces renewed scrutiny over Mauritius-linked shareholders, beneficial ownership, past stake sales, and what its eventual public listing may reveal.

The NSE Mauritius Files have placed the National Stock Exchange of India at the centre of a major debate over ownership, transparency, and regulatory accountability.

The issue concerns not only valuation, but who ultimately benefited from early and offshore shareholding in India’s most powerful financial-market infrastructure institution.

NSE was never merely a company. It was built through deliberate policy choices during India’s financial-sector transformation and post-liberalisation market reforms.

Successive governments, finance ministries, public institutions, and regulators helped create an exchange designed to replace older broker-dominated trading systems with modern infrastructure.

By the end of the UPA era, NSE had become structurally dominant, especially in electronic trading, derivatives, institutional participation, and market technology.

That dominance now forms the background to a larger question: whether offshore Mauritius vehicles quietly accumulated valuable stakes behind unclear beneficial ownership structures.

NSE’s rise from market reform project to financial powerhouse

The National Stock Exchange was created as a clean break from the older exchange order, especially the broker-club culture associated with Dalal Street.

Its stated institutional promise was transparency, demutualised governance, rules-based trading, technology-led access, and a market structure less dependent on personal relationships.

Over time, NSE became India’s most systemically important exchange, controlling critical trading infrastructure and shaping the country’s securities-market ecosystem.

Its growth was not only the result of competition. It was also enabled by regulatory decisions that strengthened its position over rivals.

The raw investigation argues that NSE’s monopoly-like strength was protected by policy conditions that made meaningful competition extremely difficult.

This matters because investors who entered early were not simply buying a financial company. They were acquiring exposure to market infrastructure.

In 2015, IFCI reportedly sold 1.5 per cent of NSE to DVI Fund Mauritius at ₹3,900 per share.

That transaction valued NSE at roughly ₹17,500 crore, according to figures cited in the investigative material reviewed for this article.

Today, the unlisted market reportedly values NSE near ₹5 lakh crore, implying an extraordinary rise in value over roughly a decade.

Such appreciation does not automatically suggest wrongdoing. However, it raises legitimate questions about valuation, timing, buyer identity, and institutional decision-making.

Also Read: Kanakia Paris Faces MPCB Scrutiny Over STP Issues.

IFCI, DVI Fund Mauritius and the valuation gap

The IFCI-DVI Fund Mauritius transaction has become central because it captures the scale of value that early NSE shareholders potentially gained.

A stake sold at a valuation of about ₹17,500 crore is now linked to an exchange reportedly worth nearly ₹5 lakh crore.

If an investor understood that NSE’s dominance would remain protected, the commercial incentive to acquire exposure was exceptionally strong.

If that exposure was acquired through a Mauritius vehicle, the question of ultimate beneficial ownership becomes even more important.

The issue is not whether foreign investment is illegal. Foreign institutional participation has long been part of India’s capital-market development.

The concern is whether some ownership structures may have concealed the real economic beneficiaries behind corporate names registered offshore.

Sprouts News presents this as an investigative hypothesis requiring official scrutiny, not as a judicial finding against any named shareholder.

A transparent regulatory review would help distinguish legitimate foreign investment from any possible nominee, conduit, or benami ownership arrangement.

Co-location case, SEBI probe and Chitra Ramkrishna controversy

The first major governance rupture came in 2015, when a whistleblower complaint alleged preferential access to NSE’s co-location systems.

The complaint alleged that certain brokers received faster market-data access, allowing millisecond advantages that could compound across high-volume trades.

SEBI investigated the matter, and the CBI later entered the case as concerns widened around market fairness and institutional governance.

Former NSE chief executive Chitra Ramkrishna resigned, and later proceedings revealed another extraordinary episode involving confidential exchange information.

SEBI proceedings stated that Ramkrishna had allegedly shared a confidential exchange strategy with an unnamed “yogi” through personal email communication.

That disclosure raised serious questions about internal controls, board oversight, information security, and the broader governance culture inside NSE.

This does not prove wrongdoing by Mauritius-linked shareholders. Yet it strengthens the case for examining governance failures alongside ownership opacity.

If confidential institutional information could allegedly move outside formal systems, regulators may reasonably ask what other undisclosed relationships escaped detection.

Citigroup Strategic Holdings Mauritius exited before the IPO

In March 2021, Citigroup Strategic Holdings Mauritius reportedly sold approximately 1.64 per cent of NSE through the unlisted market.

The deal was valued at roughly ₹1,200 crore, and portfolio rebalancing was cited as the official explanation for the exit.

Portfolio rebalancing is common among global investors. Large institutions frequently adjust holdings based on liquidity, strategy, and capital-allocation priorities.

However, the timing drew attention because NSE’s public listing had been expected for years and remained commercially significant.

A public offering could have offered better liquidity, wider price discovery, and potentially stronger valuation for a patient institutional investor.

Instead, Citigroup Strategic Holdings Mauritius exited before the IPO, before listing-level disclosures, and before deeper scrutiny of the shareholder register.

That timing is not legal proof of misconduct. However, it is a significant factual event requiring closer regulatory and market examination.

When a major offshore shareholder exits before a long-delayed listing, the question becomes what commercial, regulatory, or disclosure concerns shaped that decision.

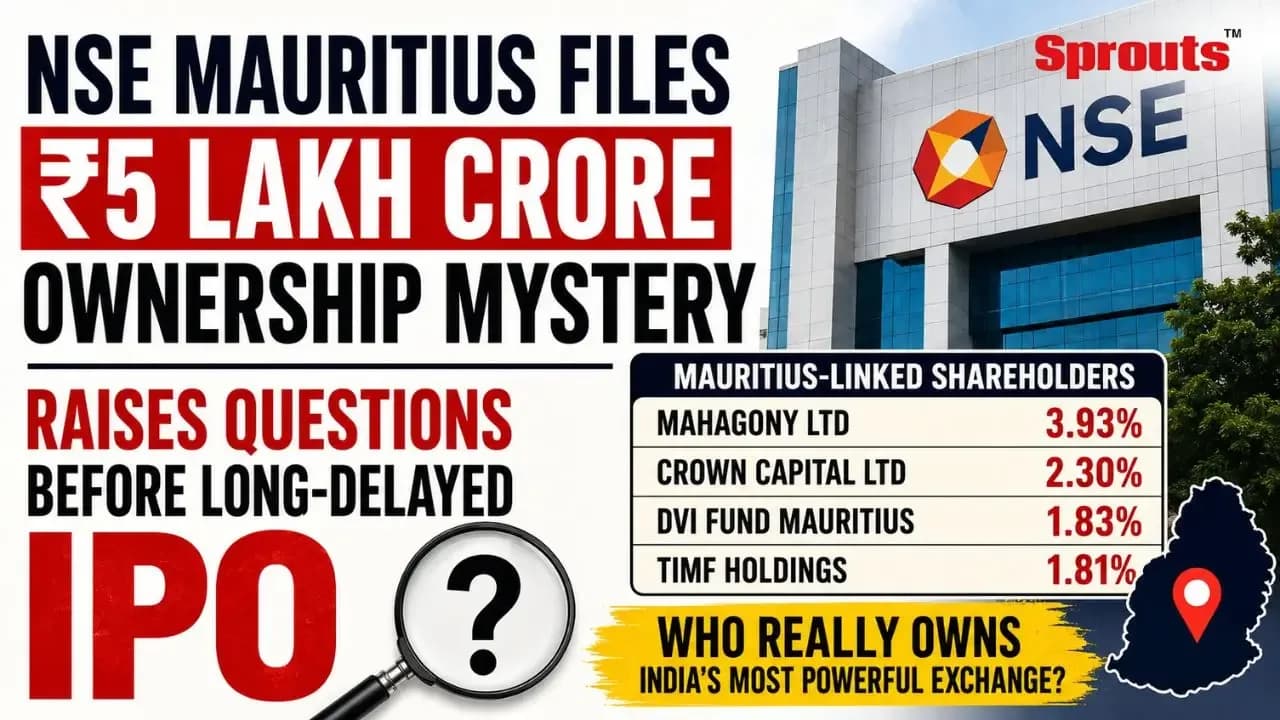

Mahagony, Crown Capital, DVI Fund and TIMF Holdings under focus

Not every Mauritius-linked shareholder exited NSE. Several entities reportedly continue holding valuable positions in the exchange’s unlisted equity.

Mahagony Ltd reportedly holds approximately 3.93 per cent of NSE, worth nearly ₹20,000 crore at a ₹5 lakh crore valuation.

Crown Capital Ltd reportedly holds approximately 2.3 per cent, representing about ₹11,500 crore under the same valuation benchmark.

DVI Fund Mauritius reportedly holds about 1.83 per cent, valued near ₹9,150 crore based on current unlisted market estimates.

TIMF Holdings reportedly holds approximately 1.81 per cent, adding another estimated ₹9,050 crore to the unresolved ownership question.

Together, Mahagony Ltd, Crown Capital Ltd, DVI Fund Mauritius, and TIMF Holdings represent nearly ₹50,000 crore of NSE-linked wealth.

The concern is that these are corporate names connected with Port Louis, while their ultimate beneficiaries are not publicly known.

Four Mauritius-linked names holding tens of thousands of crores in India’s most important exchange create a serious transparency challenge.

Why the NSE IPO could force disclosure

NSE’s eventual IPO would not merely be a financial event. It would also be a major disclosure event.

Public listings require deeper scrutiny of shareholders, risk factors, material litigation, governance structures, related parties, and beneficial ownership.

For transparent institutional holders such as Temasek and Canada Pension Plan, disclosure is generally less complex because their identities are already public.

For Mahagony Ltd, Crown Capital Ltd, DVI Fund Mauritius, and TIMF Holdings, the position appears materially different.

A public listing could require these shareholders to disclose who ultimately stands behind their valuable NSE equity positions.

Alternatively, any pre-IPO exit by such shareholders may become one of the most revealing developments in Indian capital-market history.

Such an exit would not prove illegality. Still, it could indicate reluctance to face the transparency expected in a listed company.

The listing will therefore test not only NSE’s valuation, but whether its ownership can withstand public and regulatory examination.

Supreme Court, Tiger Global-Flipkart and Mauritius conduit questions

The raw investigation refers to the Supreme Court’s January 2026 judgment in the Tiger Global-Flipkart matter involving Mauritius vehicles.

According to the source material, the ruling added legal importance to substance-over-form scrutiny of offshore structures and alleged conduit arrangements.

That ruling did not target NSE shareholders and should not be read as a finding against Mahagony, Crown Capital, DVI Fund, or TIMF.

However, it reportedly changed the broader legal environment in which Mauritius-linked investment structures are assessed by authorities.

If an offshore vehicle lacks real commercial substance, regulators may examine whether it merely conceals the actual economic beneficiary.

That principle is highly relevant where Indian assets of enormous value are held through layered or opaque offshore structures.

For NSE, the key question is whether Mauritius-linked shareholders are ordinary foreign investors or vehicles masking undisclosed beneficial owners.

That question requires documentary investigation by SEBI, enforcement agencies, company-law authorities, and other competent institutions.

The benami ownership hypothesis

The most sensitive hypothesis is that NSE may represent India’s largest unresolved benami ownership question in financial-market history.

This is a hypothesis, not a fact, and no individual or entity should be presumed guilty without lawful findings.

The concern is whether Indian insiders, conflicted actors, policy-linked figures, or legally vulnerable beneficiaries may have held stakes indirectly.

If proven, such a structure would raise serious issues under securities law, tax law, anti-benami law, and public-policy principles.

The incentive was overwhelming because NSE’s protected position made early exposure to equity potentially one of India’s greatest investment opportunities.

The mechanism was available because offshore vehicles can create distance between the registered shareholder and the final economic beneficiary.

The oversight appears questionable because ownership questions persisted through the co-location scandal, governance proceedings, IPO delays, and shareholder exits.

This combination of incentive, mechanism, and limited public transparency is why the issue demands formal scrutiny rather than speculation.

What authorities should examine next?

SEBI, the Finance Ministry, enforcement agencies, and company-law regulators may need to review NSE’s historical share transfers.

That review should examine valuation reports, buyer due diligence, board approvals, beneficial ownership declarations, and politically exposed links.

Authorities should also examine whether any public institutions sold NSE stakes at valuations that failed to protect public value.

The sale of IFCI to DVI Fund Mauritius warrants scrutiny, given the latter's valuation expansion.

Investigators should distinguish legitimate foreign investment from nominee ownership, conduit structures, or any arrangement designed to hide beneficial owners.

The objective should be transparency and market confidence, not presumption, political targeting, or reputational damage without evidence.

NSE is not an ordinary company. It is a financial-market infrastructure institution central to India’s trading, liquidity, and investor confidence.

Its ownership must therefore meet a higher standard of clarity than ordinary private commercial shareholding.

The names, the silence and the ₹5 lakh crore test

India built NSE to replace insider-driven exchange culture with transparent, technology-led, rules-based market infrastructure.

Yet the exchange’s unlisted ownership history now raises uncomfortable questions about opacity, offshore accumulation, and public-institution stake sales.

The final test may arrive when NSE moves closer to its long-delayed public listing, and listing disclosures become unavoidable.

If Mauritius-linked shareholders remain, the market may finally learn who stands behind their valuable equity positions.

If they exit before listing, that silence may become as important as any names formally disclosed later.

The ₹5 lakh crore question is not only what NSE is worth. It is who ultimately stood behind that wealth.

Reader Appeal

If you possess credible documents, records, correspondence, ownership details, transaction papers, regulatory filings, or firsthand information related to the NSE Mauritius ownership issue, offshore shareholders, beneficial ownership, or connected financial dealings, please share them confidentially with Unmesh Gujarathi. Your inputs can support responsible public-interest journalism and help bring greater transparency to this important matter. Contact: 9322755098.